7 Habits to long term wealth creation

Holi is a festival of colours. It’s a festival of joy and people spread joy by smearing each other with colours. When I talk of colours, the first thing that comes to my mind is the rainbow. People love the rainbow in the sky and it just portrays that human beings love colours and coming to think of it, I feel one always enjoys the company of people who lead a colourful life.

Holi is a festival of colours. It’s a festival of joy and people spread joy by smearing each other with colours. When I talk of colours, the first thing that comes to my mind is the rainbow. People love the rainbow in the sky and it just portrays that human beings love colours and coming to think of it, I feel one always enjoys the company of people who lead a colourful life.

Rainbow consists of 7 colours, namely, Violet, Indigo, Blue, Green, Yellow, Orange, and Red. But to lead a colourful life, one needs to have enough wealth so that you need not stress yourself out for the need for money. Human beings’ needs are ever-growing and my late father used to say that though money can’t buy you happiness it does get you food on the table and help you buy the medicines. So money can’t buy you everything but it does buy you something. Hence to have a very colourful life you need to create enough wealth so that you do not need to wake up every day and do the jobs which you probably do not like to do. Once you have that wealth, you can lead a life of self-actualization wherein you get up every day and do what your heart desires to do and lead a life of fulfillment.

Just like Rainbow has 7 colours, here are the 7 must-have habits that you can build to create long-term wealth for yourself and your family.

Just like Rainbow has 7 colours, here are the 7 must-have habits that you can build to create long-term wealth for yourself and your family.

1. Live Frugally

Just as I said above, human needs can be very aspirational but the fact is that if you decide to live a life within your means and don’t overspend, you will be able to garner enough wealth in the long term to live life to the fullest. I learned this the hard way myself. When I was in college, my pocket money was Rs. 2000 per month. Out of this Rs. 1600 used to be spent on rent and food and I had Rs. 400 for myself to take care of my personal stuff. It was difficult but I learned to manage. When I got my first job, my salary was Rs. 4,500 per month and what I did first was to buy a bike for which I ended up paying an EMI of Rs. 1800 per month. How dumb of me that in place of saving, I ended up paying the additional money on a materialistic need. I had learned to live within Rs. 2000 per month and there was an opportunity to save money but I ended up adding to my expenses. It was not only the price of the bike that hurt me but the fuel that went into it also added up plus the maintenance after a few months. So, you see it’s important that you live within your means because that’s how you will be able to garner wealth in the long term.

Whenever you feel the need for buying anything, first ask yourself if you can live without it for 3 months. If the answer is yes then put that expense out of your head for 3 months. Two things happen in such a scenario:

- You save in these 3 months

- After 3 months you might realise you do not need it.

This is how you can curb your spending habits. We are living in the world of social media and the FOMO effect (Fear Of Missing Out) makes many of us buy stuff that we might not have done. Living frugally is a good habit and it’s important to keep doing that because the savings build up over time and your goal of financial freedom will come that much closer.

2. Invest First, Savings Next, Expense Last

Now that we spoke about living frugally, what do we do with the extra money that we have in hand? People keep it lying in their savings account. It’s still better than spending it but one needs to remember that your money doesn’t grow in banks. Well, it does but it doesn’t cover inflation in the long run. So, you should plan up your investment first.

Start with the 80-20 rule if you have not yet started this habit. It means, 20% of your earnings will be for investments. Over a period of time, once you build up the habit, you can increase it. It doesn’t mean you should spend the other 80% though because 10% you should keep for emergencies. Try and lead your life with 70% of your earnings. As I wrote earlier, when we start, our needs are less, it’s just that over a period of time we keep adding our expenses. But if you have a frugal mindset, you won’t do that and if you have the goal of financial freedom and dream of living a colorful life in the future then you need to build up this habit as soon as possible.

Now, investments are of various kinds, Gold, Real Estate, Mutual Funds, Fixed Deposits, PPF, Stocks, etc. and I will come to it in detail later but for now make it a habit and mark it in your calendar that 20% of your earnings are to be earmarked for investments.

3. Insurance

If you are married or about to be married then the first thing you need to do is to buy a Life Insurance Policy. Do not fall for the various endowment schemes that all Life Insurance companies have, just buy a term life insurance policy. Now the question that will come to your mind is how much you should insure yourself for? Well, the thumb rule is, to buy a policy with a sum assured of 10 times your NET Annual income. So if you are earning, for example, Rs. 3 Lakhs per annum then purchase a policy of Rs. 30 Lakhs. As your income grows you need to increase the sum assured too by purchasing additional policies.

Other than a life insurance policy, you need to have health insurance too. Today health expenses have gone pretty steep and you must cover yourself and your family well in this regard. Never disregard this because at a younger age people feels that insurances are an additional burden on the expenses but believe me if you purchase a policy early on in your career, then the premiums are pretty low and do not increase by leaps and bounds than if you purchase a policy for the first time in the middle age.

Remember this golden rule, that insurances are not your investments but it does help you in getting tax rebates. Also never start a family without having yourself properly insured. Start a recurring deposit with your bank so that you do not feel the pinch of paying the premiums at the end of the year.

4. Short Term and Long Term Goals

What are your goals? What is your ambition? What is your dream? These are some questions which you should ask yourself quite early in your career. Also equally important is to write down the goals and give a timeline to each of the goals. Once you give a timeline, you get a deadline for yourself and when you give a deadline you can then plan on how to reach there within the specified time.

What are your goals? What is your ambition? What is your dream? These are some questions which you should ask yourself quite early in your career. Also equally important is to write down the goals and give a timeline to each of the goals. Once you give a timeline, you get a deadline for yourself and when you give a deadline you can then plan on how to reach there within the specified time.

Long-term goals can be achieved only by passing through short-term goals. So other than the long-term goals have a few short-term goals too because when you reach those short-term goals you will get extra motivation to reach your long-term goals. Also by reaching your short-term goals you will start having confidence that you are on the right track towards financial independence.

Now, what are short-term goals? It could be your younger sister’s marriage in 3 years? It could be your son’s admission to school? You define your goals and then plan how you can reach them. Always have a budget and while calculating keep inflation in mind. While budgeting, keep it on the higher side so that you do not get last-minute surprises. Once again everything starts with the habit of living frugally. If you do not curb your expenses, you will never be able to reach your goals. Expenses find their way of creeping up but if you are focused on attaining your goals then nothing can stop you from living frugally and within your means.

5. Assets

Your net worth is (Asset – Liabilities). So if you focus on increasing your assets without increasing your liabilities, your net worth will soar and one day you will be able to reach your goal of financial freedom and colourful life. Assets cannot be built overnight. I remember as a kid I used to live in a rented house for close to 16 years. After that, my father bought a piece of land and then built a house on that land after a year, and finally, he had his first asset. It was a very happy day for him because years of hard work went behind having his own property – a property built fully on cash, nothing on debt. This is only possible if you have a frugal lifestyle. Each penny saved is each penny earned. Keep faith in this theory. Today loans are very easily available and most of us buy cars, properties on loans. But if you do a small calculation you will understand that you are paying much more than what the asset is worth in terms of interest. Remember inflation is only going northwards so your net worth is going to fall if you believe that increasing your assets by taking loans is a good strategy. It never was and it never is. Many people will tell you that buying a car by taking a loan is not a good idea but buying a house on loan is a great idea. It’s not because no one can predict the future and if something untoward happens then quickly this asset would become a liability.

So purchase and build up your assets by liquidating your investments but only when you are reaching your goals. This is exactly the reason why I advised above about writing down the goals. After writing down the goals, keep monitoring the progress.

What I do is, I have a master excel sheet (google sheet) which is shared with my wife where I keep a track of all my investments. The sheet has many tabs with each tab being one goal. Each goal then has a target figure (amount) along with a date by which I need to reach the goal. Then every year, I update that sheet and see how far we have progressed across each goal. Thereafter we plan the next year. It’s a simple habit which anyone can follow which in the long run will give you great benefits.

I have seen people who get a good raise and immediately end up spending the extra cash. This is a very bad habit. Remember the 80-20 rule I told you about above? Follow the same rule when you get a raise too and this way you will be able to reach your goals faster.

Assets take time to build and hence if you do not save and invest regularly you will always feel that you are not earning enough. I hear many people telling me that he or she earns very less so they can’t save or can’t invest but that’s an excuse because it’s your habit that is stopping you from investments and savings. First, build the habit of living frugally and then start investing right after getting your paycheck. Do not look at your investments more than once or twice a year and then one day you will save enough to build your assets.

Gold is another asset that takes time to build but with the Government of India coming up with the Sovereign Gold scheme once every 2-3 months, I would suggest investing in that. If you do not have a dream of acquiring physical gold this is a good way of building your assets.

6. Equities

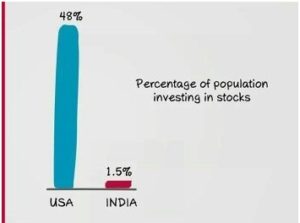

The best investment with great long-term returns is an investment in legitimate businesses. If you understand the stock market and have a Demat account then purchase good stocks and hold them for the long term. Long-term means 10-15 years. Do not buy stocks based on tips. Only invest in businesses that you understand. I generally do not invest in more than 4-5 stocks at a time. I have made mistakes too when I did not understand the markets properly and ended up losing money. Never buy stocks based on the stock price. Buy stocks based on the value of the business. If you do not understand the stock market, then start reading some books. One of the best books that I can recommend in this field is The Intelligent Investor by Benjamin Graham. The fact of the matter is that you will have to learn the tricks of the trade if you wish to retire wealthy and retire early. When I talk of early retirement, I am talking of retirement from your daily grind. Once you are financially independent, you can then do stuff that you love to do or follow the passion that has long been hidden inside you. Remember one thing, stay away from negative people because when you enter the stock market you will get a lot of advice, and mostly the advice would be about the stock market being a gambler’s market. It’s wrong because it’s gambling only when you are trading daily but here we are buying businesses for the long term to build up our assets and increase our net worth.

The best investment with great long-term returns is an investment in legitimate businesses. If you understand the stock market and have a Demat account then purchase good stocks and hold them for the long term. Long-term means 10-15 years. Do not buy stocks based on tips. Only invest in businesses that you understand. I generally do not invest in more than 4-5 stocks at a time. I have made mistakes too when I did not understand the markets properly and ended up losing money. Never buy stocks based on the stock price. Buy stocks based on the value of the business. If you do not understand the stock market, then start reading some books. One of the best books that I can recommend in this field is The Intelligent Investor by Benjamin Graham. The fact of the matter is that you will have to learn the tricks of the trade if you wish to retire wealthy and retire early. When I talk of early retirement, I am talking of retirement from your daily grind. Once you are financially independent, you can then do stuff that you love to do or follow the passion that has long been hidden inside you. Remember one thing, stay away from negative people because when you enter the stock market you will get a lot of advice, and mostly the advice would be about the stock market being a gambler’s market. It’s wrong because it’s gambling only when you are trading daily but here we are buying businesses for the long term to build up our assets and increase our net worth.

Even after all this if you feel uncomfortable entering the stock market right away, start with investing in mutual funds. Have a basket of mutual funds (Large Cap, Mid Cap, Small Cap, Balanced and Diversified Equity). You can also invest in Index funds. Take the SIP route to start your investment journey. When I started investing in mutual funds (I am a late learner and a late groomer) we did not have the opportunity of directly investing in the mutual funds and had to take the route of investing through the mutual fund agents. Things have changed now and you can invest directly online. This will save you some extra money which in effect goes to the agents. Once again, most of these investments can be easily liquidated and hence resist looking at your profit/loss regularly. Once in 6 months is more than enough to see how things are shaping up. If you are new to this, start with Large Cap, Diversified Equity, and Index Funds. These are relatively less volatile than small-cap and mid-cap funds. One necessary caution, do not be overly aggressive. Build your portfolio slowly but stay put.

7. Debt Free

I already touched on this point earlier that building assets via debt (loans) is never a good strategy. The profit that you build up with your investments can be completely wiped out due to the debts. Remember, Assets – Debts (Liabilities) = Your Net Worth. So keep debts at the bare minimum and keep increasing your investments to improve your net worth.

My father always told me that he might not be able to leave me with a lot of cash but he will ensure that he will never keep any debt on my head and that’s what should be the motto for everyone too. No one knows the future and building up an asset class by increasing debt might end up putting you and your family in despair in the future. To get a good night’s sleep get rid of your debts today. If you have already taken a lot of loans then first create a plan on how you are reducing them. Maybe as per the 80-20 rule, when you get a raise, in place of investing the new 20%, service your debt instead.

These are some tips if you follow diligently will lead you to financial freedom. Once you have your financial freedom, you will see this world in a different light and your life will be colourful too.

So what are you waiting for? Start planning today!

Wishing you all a very happy and colourful Holi. Last year we didn’t celebrate Holi due to Covid-19 and nothing has changed this year too as new cases keep rising once again. So stay safe and enjoy your day with your family.

Wishing you all a very happy and colourful Holi. Last year we didn’t celebrate Holi due to Covid-19 and nothing has changed this year too as new cases keep rising once again. So stay safe and enjoy your day with your family.

Till we meet again, take care and God bless!

Recent Comments

Related blog posts

Why do we love weekends?

TGIF was the name of a restaurant in Koramangala in Bangalore (not sure if it still exists). When I first saw that restaurant back in the mid-'90s, I

Read More

Are you enjoying your freedom?

Today is 15th August 2021 and we celebrate our 75th Independence Day. India has come a long way from 1947 when Pandit Jawaharlal Nehru hoisted the tr

Read More

Save First and Spend Later

“I have so many expenses. I can’t save money with the salary I get currently.” - one of my colleagues told me this. Believe me, if you are havi

Read More

The journey is yours – The rest can chill

All our lives we keep trying hard to impress others! As a child, we want to impress the teacher! The seed is sown. Then you see your parents trying

Read More

Ordinary Habits! Extraordinary Results!

Read 25 pages a day and you will end up reading 36 books in a year. Write one page a day & you will be able to publish a book at the end of the y

Read More

Fantastic

It is very important and helpful. article.

Thank you